Assessment Information

ASSESSOR< back to Assessment Data

As an elected official, the County Assessor’s principal function is to assess all property, not expressly exempt, within the county at market value and to maintain records of ownership of all property within the county. Each year, assessment notices are sent to all property owners to make them aware of the information on file concerning their property.

The links below offer information on how the Assessor collects, calculates, maintains and distributes this information. You will also find information on when to expect mailings from the Assessor and deadlines to respond to those mailings. If you have any questions, please contact the Canyon County Assessor at: 2cAsr@canyoncounty.id.gov

- Appeals Process

- Appeal History

- Determining Property Taxes

- Important Dates

- Citizen's Guide to Property Assessment

As a property owner, nobody is more knowledgeable about your property than you. The purpose of the assessment notice is notify you of the information the county has about your property. If changes need to be made to the assessment, you must contact the Assessor’s office before the deadline printed on the notice. Although this notice is not a bill, nor does it inform you of what your bill will be, it is very important that you read it carefully. By the time you receive the bill, it will be too late to make changes to the assessment.

What are the grounds for an appeal?

There are provisions in Idaho Code to appeal only assessments. Taxes can not be appealed. An assessment appeal is an attempt to prove that your property’s estimated market value is either inaccurate or unfair. It is not a complaint about higher taxes.

You may appeal when you can prove at least one of the following:

- Items that affect value are incorrect on your property record. Examples may include having one bath, not two. They might also include you having a carport, not a garage, or your home having 1,600 square feet versus the assessed 2,000 square feet.

- The estimated market value is too high. You have evidence that similar properties have sold for less than the assessed value of your property prior to January 1 of the current year.

NOTE: You will not win an appeal because you think your taxes are too high. This is an issue you must take up with the elected officials who determine budgets. However, you may be eligible for tax relief or exemptions. Information about these exemptions can be found on this site under the heading Property Tax Relief.

The Appeals Process – Step-By-Step

There is only one time of year that assessed values can be appealed. This is when the assessment notice is mailed out. The majority of property is on the regular roll and those assessments are mailed out the beginning of June each year. When you receive your assessment notice, read it for instructions about deadlines and filing procedures. If they are not clear, contact the Assessor’s office for more information. Be sure you understand and follow the instructions. A missed deadline or incorrect filing can cause an appeal to be dismissed.

Informal Review

The first step in an appeal is an informal meeting with a Deputy Assessor (generally the county appraiser assigned to your area). Sometimes this informal review is handled by telephone or email.

Preparing for Your Appeal

Prepare for the meeting. Find the account (parcel) number on your assessment notice in the upper right hand quarter of the assessment notice. Use this number to view or obtain a copy of your property record from the Assessor’s office or database located on this website ![]() . Review the facts on the property record. Is the architectural style correctly listed? If not, a recent photo of your home will help correct the information. Check the living area of your home, the size of your lot, the number of bathrooms, the presence or absence of a garage or finished basement, the year built, the construction materials, the condition, and so on.

. Review the facts on the property record. Is the architectural style correctly listed? If not, a recent photo of your home will help correct the information. Check the living area of your home, the size of your lot, the number of bathrooms, the presence or absence of a garage or finished basement, the year built, the construction materials, the condition, and so on.

Gather as much information as you can on similar properties in your neighborhood, especially those that have recently sold. Ask your real estate broker for sales prices on these properties. Remember, only arms-length transactions that completed prior to January 1 of the current year can be used. Use the Assessor’s maps ![]() and this website

and this website ![]() to review comparable property record forms, which should also show their appraised values. You may also wish to use the public computers located in the Plat Room Room 230 in the Administration Building. Compare the features of these properties to the features of yours. A difference in features may result in a difference in values.

to review comparable property record forms, which should also show their appraised values. You may also wish to use the public computers located in the Plat Room Room 230 in the Administration Building. Compare the features of these properties to the features of yours. A difference in features may result in a difference in values.

The Meeting

The purpose of the informal review (which is not yet an appeal)— should be:

(1) To verify the information on your property record form

(2) To make sure you understand how your value was estimated

(3) To discover if the value is fair compared with the values of similar properties in your neighborhood.

(4) To find out if you qualify for any exemptions.

(5) To verify that you understand how to file a formal appeal, if you still want to. Most disputes are a result of misinformation on one side or the other and are resolved in this meeting.

The person conducting the meeting will review your property record with you and give you information about comparable properties. Present any information you have gathered at this time.

The person conducting the meeting may not commit to a change in value at this meeting, even if you may have uncovered an error or the assessment appears to be inequitable. The decision about a value change may have to be made by someone else and communicated to you in writing. Most often, a corrected assessment notice can be mailed within 2-3 weeks.

View the Assessors’ office as an ally, not an adversary. Staff at the office have been trained to be helpful, calm, and polite, but they are only human. If you can remain calm and polite, they can more easily concentrate on giving you the information that you need.

Formal Appeal

If you are not satisfied with the results of your informal review, you still have options. The next step is a formal appeal before the Board of Equalization. To be scheduled for an appearance before the board of equalization you must file an appeal in writing on a form provided by the Assessor’s office. This form is obtained from the person that conducted the informal review. See Idaho Code 63-501A.

Your appeal is more likely to be successful if you present evidence that comparable properties in the same neighborhood as your property have sold for less than your assessment in the previous year (sales occurring after January 1 of the current year are not admissible). Comparable properties will have the same or similar: attributes, building size, year built, lot size, bedroom and bathroom count, and be in the same or similar condition as your home. Copies of property records on your comparables with sales prices are your best defense. Note any differences between your property and the comparables and point out these differences. An appraisal of your own property, presenting the value as of January 1 of that year, may also be good evidence. The Board of Equalization will be interested only in the fairness and accuracy of the value placed on your property, not whether you can afford to pay your tax or whether taxes are too high. There are other avenues to address those issues. See Idaho Code 63-502.

If you disagree with the local board’s decision, additional levels of appeals are available with the State Board of Tax Appeals ![]() , and subsequently in District Court. Information about these procedures are available from the Commissioner’s office. See Idaho Code 63-511.

, and subsequently in District Court. Information about these procedures are available from the Commissioner’s office. See Idaho Code 63-511.

Any other questions can be directed to the Canyon County Assessor at 2cAsr@canyoncounty.id.gov

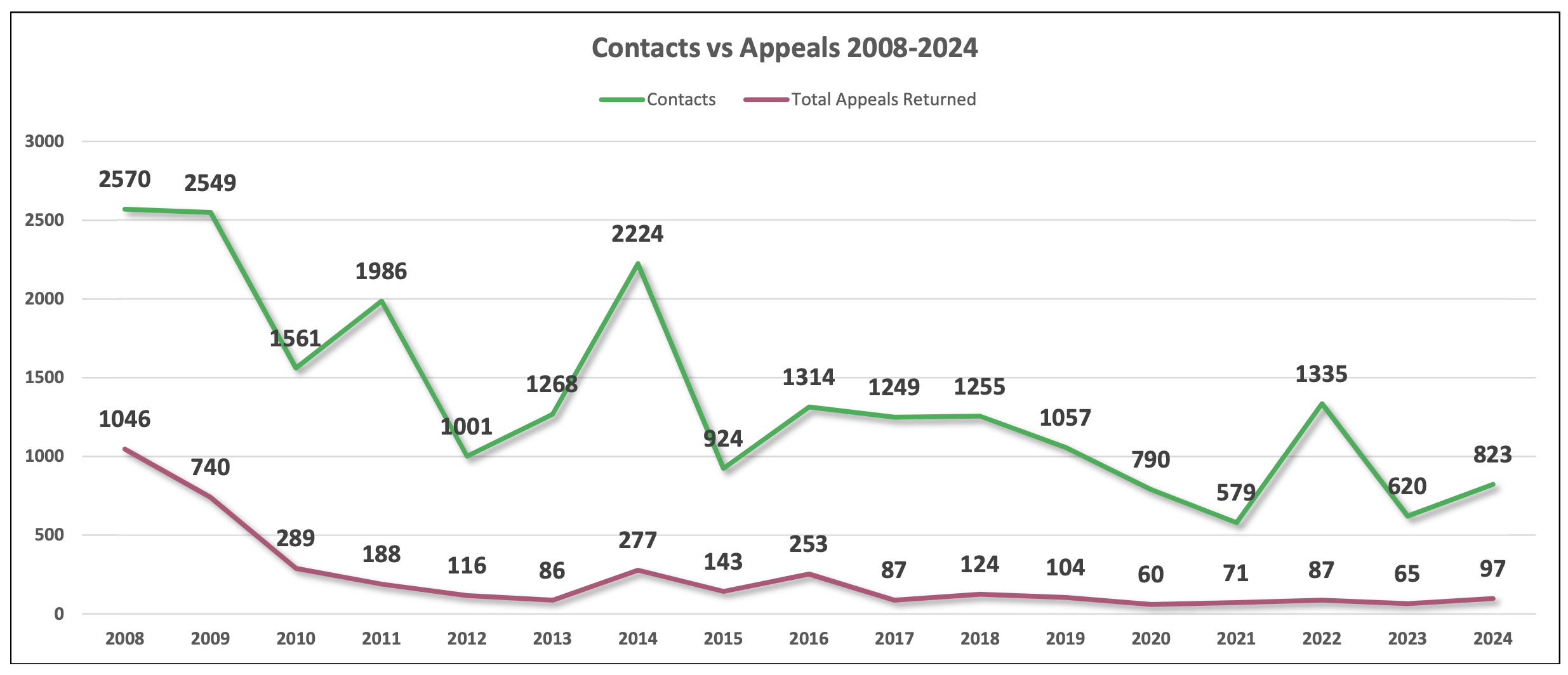

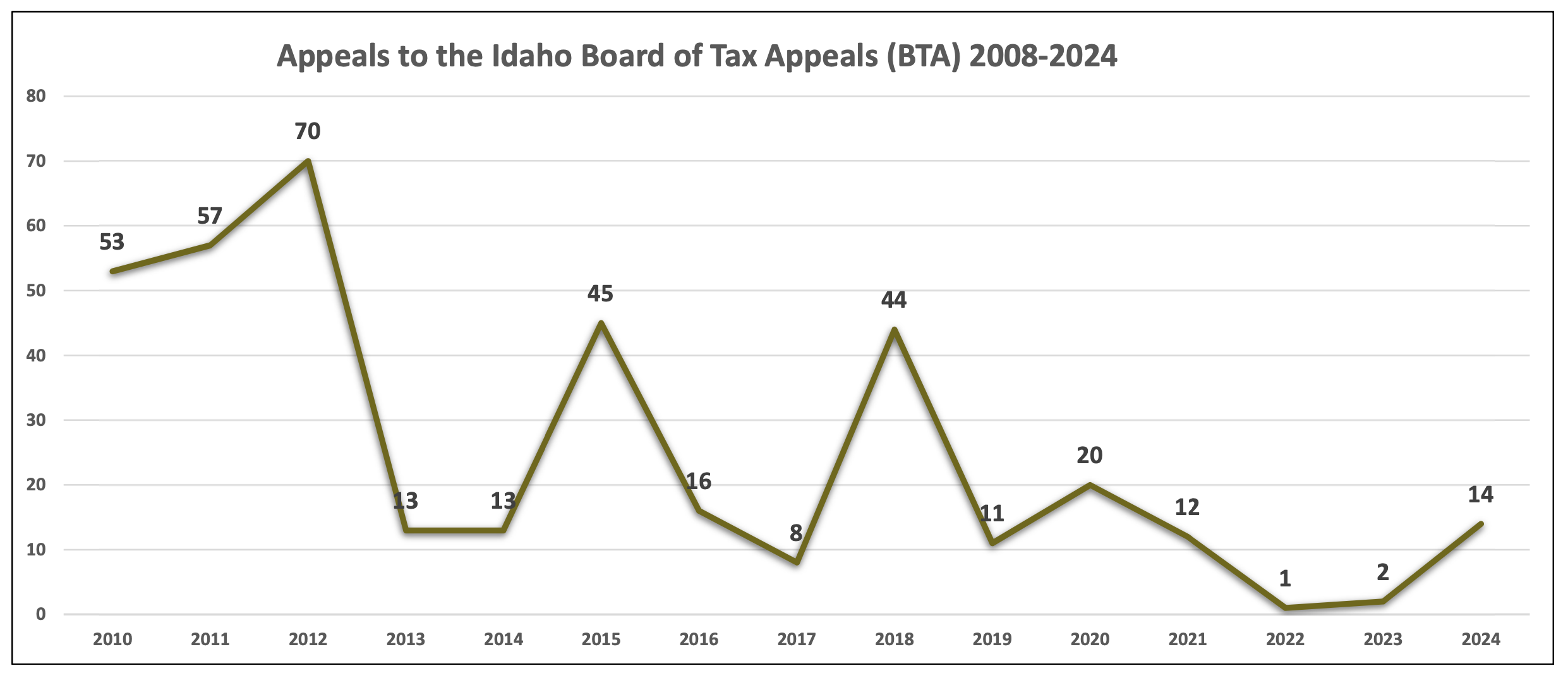

Understanding Appeal Season Trends

The graph below depicts the relationship between customer inquiries and appeals during our annual appeal season. We track all customer contacts, which include phone calls, emails, and in-person visits, related to assessment notices. These inquiries are logged as “contacts” in our system.

The graph will show the total number of contacts we receive each year compared to the number of completed appeal forms submitted during the corresponding appeal seasons. This data can help us identify trends and adjust our resources to better serve our customers.

Determining Property Taxes

Many people mistakenly think the change in their assessed value is a direct link to what will happen with their property taxes, but property taxes are budget driven not assessment driven. This means that all property values could stay exactly the same and property taxes could still increase because of budget increases. There is a cap to budget increases which is discussed in more detail here. It is important to note that property taxes are the principal source of income for cities, counties and special-purpose governments like fire, schools, library,cemetery and other districts. These taxing districts provide vital services for our citizens, many of which are required by law regardless of the funds available. See Required County Services.

When it comes to property taxes there is a confusion of the duties of the Treasurer and Assessor since they are so closely related. The county Treasurer sends the tax bills, receives tax payments, then distributes it to the taxing districts. The Assessor’s job is to make sure homes and businesses are valued correctly for the purpose of calculating each owner’s tax bill. Under Idaho Code 63-205, the assessed value must be the same as the actual market value of that property as it is on January 1st. As mentioned, the assessed value helps determine the tax burden of the property owner, but it is not the only factor. Levy rates have a large impact on one’s tax bill. A levy rate is the amount multiplied by the assessed value to calculate the tax bill.

Determining Levy Rates

Taxing District Levy Example

| Budget Request | / | Property Value | = | Tax Rate (Levy) |

|---|---|---|---|---|

| $42,000,000 | / | 13.2 billion | = | .00311313 |

- Each tax district determines their budgets at public hearings. See Idaho Code 63-803

- Individual properties are assessed to determine their market value

- Homeowners (and other) exemptions are subtracted from the value

- The total budget dollars requested by each district is divided by the total taxable value in the areas they serve.

Information on taxing district’s actual budget requests are available on this website under the heading “Taxing District Budgets”. Information on how levy rates are used and how they impact the tax bill is below.

Properties are generally served by more than one tax district, so the levies of all the tax districts serving your property are added together. The geographical areas in each county having a common group of tax districts is called a Code Area. The levy for this Code Area is shown in the table below.

| a) County | 0.003113130 |

| b) School | 0.005137568 |

| c) City | 0.005811937 |

| d) Special Districts (highway, cemetery, etc.) | 0.001004090 |

| Total | 0.014062635 |

The taxable value of each property is determined:

| House Value | $200,000 |

| Land Value | $ 50,000 |

| Total Value | $250,000 |

| Minus Homeowner’s Exemption | ($125,000) |

| Total Taxable Value | $125,000 |

Individual Tax bills are calculated:

| Taxable Value | X | Levy Rate | = | Tax Amount |

|---|---|---|---|---|

| $125,000 | X | 0.014062635 | = | $1,757.83 |

The collection of unpaid balances owed to certain agencies, may be added to your property tax bill. If you have questions regarding an amount charged by an agency to your property tax bill, please contact that agency. See Idaho Code 50-1008.

At this point you may have some questions such as:

Doesn’t the law limit the amount taxes can increase?

How do property taxes increase?

What property is taxed?

These questions can be answered by following the links attached to them. Look for other questions you may have in the Frequently Asked Questions section of this site. A listing of levy rates is made available annually on the Treasurer’s department’s site.

January 1st

Lien Date. This is the date used to determine market value. Idaho Code 63-205

Tax Collector makes delinquency entry to property tax roll on properties which the first half was not paid. Idaho Code 63-907. Special provisions apply to delinquent property assessed on the personal property tax rolls. See Idaho Code 63-904.

Property Tax Reduction applications may be completed online. Idaho Code 63-706

March 15th

Business Personal Property Declarations are due. Idaho Code 63-302 (1) Agricultural Exemption Forms are Due.

April 15th

Last day to apply for Property Tax Reduction and Disabled Veterans Benefit programs. Religious, Nonprofit, School, Hospital … Exemption Forms are Due. Idaho Code 63-602(3)(b)

Third Week of May

Treasurer sends a courtesy reminder notifying taxpayer of taxes due.

First Monday in June

Assessor sends assessment notice to tax payers. Idaho Code 63-308(1)

Fourth Monday in June

Deadline to appeal the assessed values on the regular role. Idaho Code 63-501A Deadline to submit application for exemption from tax valuation. Idaho Code 63-501 (b) Deadline to submit application for casualty loss exemption. Idaho Code 63-602X

June 20

Last day to pay prior year second half tax payment without late charges and interest accruing and calculated from January first. Idaho Code 63-903(1) Assessor certifies property tax reduction roll to the County Auditor and the State Tax Commission. Idaho Code 63-707(2) Deadline to submit application for hardship exemption for the current year. This application is submitted to the Board of Equalization. Idaho Code 63-602AA

Second Monday in July

The Canyon County Commissioners must complete business and adjourn as the Board of Equalization by this date. Idaho Code 63-501 (1) second paragraph

First Tuesday in September

Board of County Commissioners adopts final county budget at public hearing. Idaho Code 31-1604

Fourth Monday in October

The State Tax Commission shall notify the County Commissioners of the approval of all levies. Idaho Code 63-809(1)

Fourth Monday in November

Tax Collector mails a tax notice to the last known address of every property owner or tax representative. Idaho Code 63-902

Assessor assesses any property not assessed by the 4th Monday in June and delivers the completed subsequent roll to the County Clerk. Assessor mails valuation notice to the taxpayer for the property on this subsequent property roll. Idaho Code 63-311(1)

December 20th

All property taxes are due and payable to tax collector on or before December 20th of the year property taxes are levied. Property taxes may be paid in two halves; the first half being due by December 20th with a grace period extending to June 20th for the second half if the first half is totally paid. See Idaho Code 63-903

How is my property assessed, why is my property’s value increasing, and what can I do about it?

Many citizens have questions about how their property is assessed and what they can do if they dispute the assessment. We at the county assessor’s office think it’s important you understand why and how assessors and their staff do their jobs, and we’d like to clear up a few misconceptions.

The duty of the assessor’s office is simply to keep the assessed value of your property as close as possible to the actual market value.

Also,older neighborhoods need extra care in valuations. In modern subdivisions, all the homes are pretty much the same size, the same age and in the same condition, which makes our job a lot easier. But the same things that make an older neighborhood so attractive and charming(the diversity of home styles, ages and appearances, and small commercial center in the neighborhood) also make its homes harder to assess, and this makes your feedback all the more crucial.

If you call our office to discuss your valuation, please read the following beforehand; it will likely answer some questions you have:

Why is my home assessed, and how?

Property taxes are a principal source of income for cities and counties and special-purpose governments like fire, schools, library, cemetery and other districts. Each of these local governments applies a tax rate to the value of your property. For example, let’s say your city levies$1.50 for every $1,000 of taxable value; if your house has $100,000 of taxable value, you would owe the city $150 a year in property tax.

The county treasurer sends you a bill and collects the tax, then distributes it to the local governments. At the assessor’s office, our job is to make sure homes and businesses are valued correctly. Under Idaho law, our assessed value must be the same as the actual market vale of that property.

To make the process as fair and consistent as possible, we use three methods to value homes:

- Annual updates. Every year, the county updates your home’s value based on the price of similar homes in the neighborhood (this is called trending).

- Five-year updates. These are more detailed than the annual updates. Once every five years, a deputy assessor walks by your property to determine if there have been any obvious additions, improvements or anything else that would affect your home’s value, such as the condition of surrounding homes.

- Citizen feedback. Citizen comment is important to us. Since we aren’t in the habit of looking in people’s homes uninvited, there are lots of things we do not know that could influence a home’s value. We want property owner to let us know if they think our valuations are too high (or too low, but not many people complain about that!). You may also ask us to visit your home and do a more detailed assessment. We may discover our assessment was too high, too low, or about right. You can appeal any decision we make to the Board of Equalization when you receive your assessment notice.

Why is my assessment going up so much?

Many things can affect the value of your home and some of them are under your control and some are not. Things you can control are the appearance and the size of your home. Things you can not control are the location and the value of surrounding homes and the general neighborhood. If a neighborhood falls into decline, its property values will decrease. But sometimes, older neighborhoods become desirable once again and are “gentrified.” While this sort of neighborhood revitalization is good, it can cause values to rise steeply in just a few years.

Also, physical appraisals are the most accurate appraisal method. The current process requires the counties to appraise all properties every 5 years. In the intervening years the counties are required to do an adjustment to ensure that all properties are at current market value.

How does my assessment affect my tax liability?

Other factors affect your tax bill, such as the addition or retirement of school bonds, local improvement districts and special levies. Ultimately, however, the free market determines your property’s value. When supply is limited and demand increases, values go up, just like any other commodity.

The effect of value increases on your property tax depends upon the rate of increase in your property value compared to the rate of increase or change in value of all other properties. If your value increases more rapidly than that of all other properties then your taxes will increase more rapidly. In any event, the increase in value does not lead to increased budgets or revenues for taxing districts. Taxes are budget driven not assessment driven.

If my home’s assessed value increases 15 percent, does that mean my taxes will increase 15 percent? Don’t local governments have a 3 percent cap on their annual budget growth, and if they do, how can my taxes go up more than 3 percent?

The assessed value of your property is not the only factor in determining your property tax liability. Your value could stay exactly the same and your tax bill could still go up (or down). For example, if every property in your taxing district increased in value the same amount and the budgets of the taxing districts stayed the same, you could expect your tax bill to stay the same. Local governments do have a 3% cap plus new construction value on their budgets. Another example is, your assessed value decreases but a special levy (such as a new school) is voted in by the public, you may see your tax bill increase. Another reason your tax bill could increase by more than 3% in one year is the value of other properties in your taxing district decrease while your value stays the same.

While no one wants to pay more in taxes, there are some good things about the value of your property increasing. For most people their home is their single most valuable possession and greater value represents greater equity. So, if you sell your home, it will be worth more, even if you did little or nothing to increase its value. (In fact, increasing homes values is one of the greatest reasons we feel good about the economy.) If you need a mortgage loan, or you need to use your home to help with retirement, you will have more equity to draw on.

Main Assessor Location

111 N. 11th Ave Caldwell

Main Assessor - Suite 250

Appraiser Room - Suite 220

Vehicle Registration Location

6107 Graye Lane, Caldwell

Vehicle Registration Online

MV@canyoncounty.id.gov

Auto License Contact

P 208-455-6020

F 208-454-6019

Main Phone / Fax

P 208-454-7431

F 208-454-7349

Office Hours

Weekdays 8am - 5pm

(excluding holidays)

DMV 8am - 4pm

(excluding holidays)